In an era of one-size-fits-all advice, truly personalizing your investments can be the difference between financial stress and lifelong confidence. A tailored portfolio adapts to your evolving needs, goals, and circumstances—offering a pathway to sustainable growth and emotional peace of mind.

Defining Your Customized Investment Strategy

A customized investment strategy reflects your unique goals, time horizon, risk tolerance and financial situation. Unlike a one-size-fits-all 60/40 stock-bond mix, a tailored portfolio incorporates your income needs, tax status, values, and legacy preferences.

Core considerations include:

- Financial objectives: retirement, education, major purchases

- Time horizons: short-term vs. long-term goals

- Risk appetite and psychological comfort

- Cash needs and liquidity requirements

- Tax situation and account types

- Personal values: ESG, legacy holdings, concentrated positions

The Benefits of True Personalization

Investing in a portfolio aligned with your real-world circumstances confers multiple advantages:

- Alignment with real-world goals keeps you focused on long-term plans and shields you from market noise.

- Risk–return fit matches volatility exposure to your tolerance and time horizon, reducing panic selling.

- Better diversification and risk management address concentrated positions and employ global allocations.

- Tax efficiency through deliberate asset location and tax-loss harvesting techniques.

- Adaptability to life changes allows timely adjustments after marriage, career shifts, or approaching retirement.

Building Blocks of a Tailored Portfolio

Crafting a personalized portfolio involves several interlocking components, each contributing to a coherent strategy.

Clarifying personal goals and time horizons is the first critical step. Define each objective—emergency fund, home down payment, retirement—assigning a target amount, deadline, and priority. Your asset mix for each goal hinges on its time frame: longer horizons generally favor equities, while shorter windows demand stability in bonds and cash.

Understanding risk tolerance and capacity distinguishes what you can emotionally endure from what you can financially absorb. Age, life stage, job security, and existing obligations shape your capacity; your comfort with market swings dictates your tolerance. Risk categories—conservative, moderate, aggressive—serve as starting points for allocation decisions.

Designing your personal asset allocation formula means blending stocks, bonds, cash, and potentially alternatives into a mix that aligns with your goals. A young investor might adopt an 80–90% equity weighting for growth, while a pre-retiree shifts toward bonds and cash to preserve capital. Alternative strategies—real estate, factor tilts, hedging—may be added when appropriate.

Diversification across asset classes and regions remains a cornerstone. Spreading investments among equities, fixed income, real assets, and international markets reduces idiosyncratic risk. Low-cost index funds and ETFs offer broad exposure without concentration in a single sector or security.

Tax, account, and implementation choices influence net returns. Tools range from mutual funds, ETFs, and separately managed accounts to direct indexing solutions. Employ strategies like tax-loss harvesting and asset location—placing tax-inefficient assets in retirement vehicles—to enhance after-tax performance.

Finally, a portfolio is never a "set and forget" endeavor. Periodic review and disciplined rebalancing ensure allocations stay true to your plan. Schedule annual check-ins or trigger reviews upon life events—home purchase, career change, birth of a child—and rebalance when drift exceeds your tolerance thresholds.

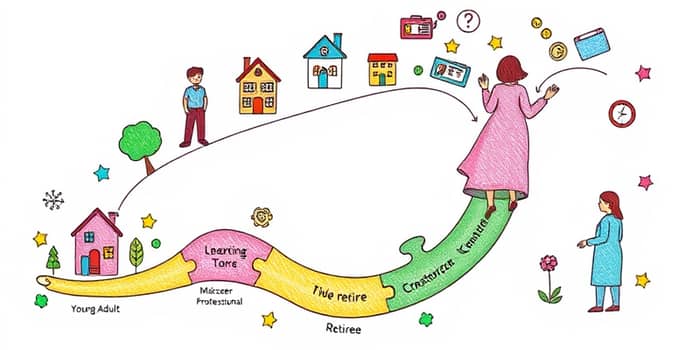

Life-Stage Tailoring: The Wealth Cycle

Your investment strategy must evolve as you progress through distinct financial life stages: Creation, Accumulation and Growth, Preservation, and Distribution. The following table summarizes key objectives and portfolio focuses at each phase.

In the Creation stage, young professionals focus on establishing disciplined saving habits, building an emergency fund, and investing early to maximize the compounding power of long-term investing. A high equity weighting and regular contributions to retirement accounts set the stage for future growth.

During Accumulation and Growth, rising incomes allow higher savings rates and more nuanced portfolios. Investors juggle multiple goals—retirement, children’s education, home ownership—often blending domestic and global equities, real estate investments, and early alternative allocations for diversification and enhanced returns.

As you enter the Preservation phase, protecting accumulated wealth takes precedence. Portfolios tilt toward fixed income and cash-sensitive instruments, while maintaining some equity exposure to outpace inflation. Hedging concentrated positions and adjusting risk profiles reduce vulnerability to market downturns.

In the Distribution stage, generating consistent income becomes paramount. Strategies include dividend-focused equities, bonds laddered for cash flow, annuities for guaranteed payouts, and systematic withdrawal plans designed to sustain your nest egg over a potentially multi-decade retirement horizon.

Across all stages, the hallmark of a personalized portfolio is its dynamic nature. Life events—marriage, job change, health concerns, inheritance—demand timely adjustments. Technology platforms and advisory services now offer increasingly sophisticated tools for real-time monitoring, automated rebalancing, and tax optimization.

Creating a truly tailored investment strategy is more than just selecting funds; it’s an ongoing partnership between your evolving life story and a disciplined financial framework. By aligning your portfolio with your deepest goals, calibrating risk to your comfort, and harnessing the power of tax-aware implementation, you position yourself not just to weather market storms, but to thrive through every stage of life.

References

- https://concenturewealth.com/blogs/personalized-investment-strategy-portfolio-optimization/

- https://www.merceradvisors.com/investing/how-to-build-an-investment-plan-for-different-life-stages/

- https://www.carsonwealth.com/insights/blog/customizing-your-investment-portfolio-the-role-of-bespoke-solutions/

- https://fctrust.com/news/investing-every-age/

- https://aiswealth.com/personalized-investment-strategies-the-power-of-a-tailored-portfolio

- https://labinsky.com/tailoring-your-finances-to-your-life-stage/

- https://www.marinerwealthadvisors.com/insights/mariner-personalized-equity-portfolios/

- https://tdwealth.net/how-to-tailor-retirement-investments-to-your-age/

- https://stevenscapitalpartners.com/unlocking-the-power-of-customized-portfolios-in-investment-management/

- https://www.youtube.com/watch?v=bINf8oUV2AA

- https://myfw.com/articles/building-a-personalized-wealth-management-strategy-key-steps-to-achieve-your-financial-goals/

- https://www.ml.com/articles/how-to-build-investment-portfolio.html

- https://www.nixonpeabodytrustcompany.com/insights/investment-strategies-for-every-life-stage